Watches Are Sports Now

On prediction markets and gambling, rankings, tribalism, and 'what it all means.'

[Note: Let’s call this an Unpolished b-side that I didn’t send as a standalone email. As you’ll see in my next newsletter, I had second thoughts about publishing (who really cares about watch futures?), but I believe the analysis adds something to the conversation.]

Like many red-blooded, especially male Americans, way too much of my brain capacity is dedicated to sports. I’m constantly checking scores, as if it really matters that my Saint Louis Billikens won by 14 last night. My Instagram feed is mostly Caleb Williams highlights, the Malice at the Palace was a seminal moment in my childhood, and I can still give you the shot-by-shot from Tiger Woods’ 2019 Masters win.

Increasingly, watches feel like sports—for better and certainly for worse.

Billionaires are buying up old watch brands the way they used to gobble up sports teams.1 We treat our favorite brands like our favorite teams, and our favorite watchmakers (or brand leaders) like our favorite players.

Take all that talk about the Morgan Stanley report

It ranks the top 50 Swiss brands by revenue and is poured over like NBA standings or NFL playoff scenarios. Tudor’s up. Omega’s down. What are they doing wrong? If I were the coach, here’s what I’d do differently.

If you own a Vacheron or Cartier, you might even feel slightly better about yourself because the brand supposedly had a good year, as if it really matters whether some Swiss company sold a few more watches. A logo and color combination give us a sense of pride, nostalgia, community, and tribalism.

Especially because watches are so expensive, we’re also mostly left watching from the sidelines. We root for our favorite teams/brands and even have schadenfreude when other ones lose. We lament bad brand management like bad play calls.

Like any good sports rankings, there’s also the reaction to the rankings. You might’ve seen Swatch Group’s letter taking issue with the annual Morgan Stanley report, but I noticed that even Tudor commented to Les Temps about its issues with the report:

“The gap between the assumptions of the Morgan Stanley study and the reality of Tudor’s business performance is so wide, year after year, that we question the relevance of the methodology and the integrity of the report’s authors.”

Harsh! Tudor also said that while Morgan Stanley attributes 70% of its business to wholesale, Tudor is exclusively wholesale.

I understand the brands’ frustrations. However, if you try so hard to keep something a secret, of course we’re gonna try to figure it out. Like with our sports teams, we feel entitled to some information about these brands we invest so much into.

The Morgan Stanley report has managed to get Swatch Group to disclose more numbers than it ever does. A little transparency is good, especially if you’re a bank writing a report mostly for professional investors.

And maybe that’s what they wanted all along?

All that to say: If any investment bank wants to partner with Unpolished and make up some rankings to shake the tree and see what falls out, you know where to find me.

Bezel x Kalshi Prediction Markets for Watches

Another way watches are now more like sports: Gambling. (Or whatever you want to call it.)

Kalshi and Bezel launched prediction markets for watches this week, a convoluted sentence that wouldn’t have made sense even six months ago and still doesn’t to Mrs. Unpolished.

Kalshi offers prediction markets to bet on elections, sports, ghoulish war trading, and now, “Watch Futures.” It’s using Bezel’s “Beztimate” data to back the markets. Kalshi has a valuation of $11b, so Bezel, and really all of watches, are a relatively small concern for a company with ambitions to let you “trade on anything.” It’s part of a larger push into collectibles by Kalshi—Labubus and Pokémon cards came before.

If you’re a Rolex Submariner, you won’t like to hear that you’re now in the same category as weird monster-looking keychains or trading cards. It was probably inevitable that prediction markets would come for watches—the only way a company like Kalshi can justify its massive valuation is to financialize culture.

And I love to place a few chips on red as much as the next degenerate, but only in Vegas or very occasionally, Rivers Casino in Des Plaines, Ill. The proliferation of gambling into every corner of culture has many saying we’re cooked.

BUT plenty of people already look at you, me, or certainly Kevin O’Leary spending untold sums on watches as a sign that we’ve been cooked. Layering prediction markets on top certainly compounds the problem, but it’s not like watches were pure as the Virgin Mary before Watch Futures came along.2

I don’t totally mind the “financialization” of watches that purists often decry. Watches have gotten expensive, and it’s reasonable to treat your watches, if not like assets, at least something akin to a store of value—no one wants to lose a bunch of money on a Blancpain Villeret Triple Calendar and be taken for a fool (I hope you got a discount!).

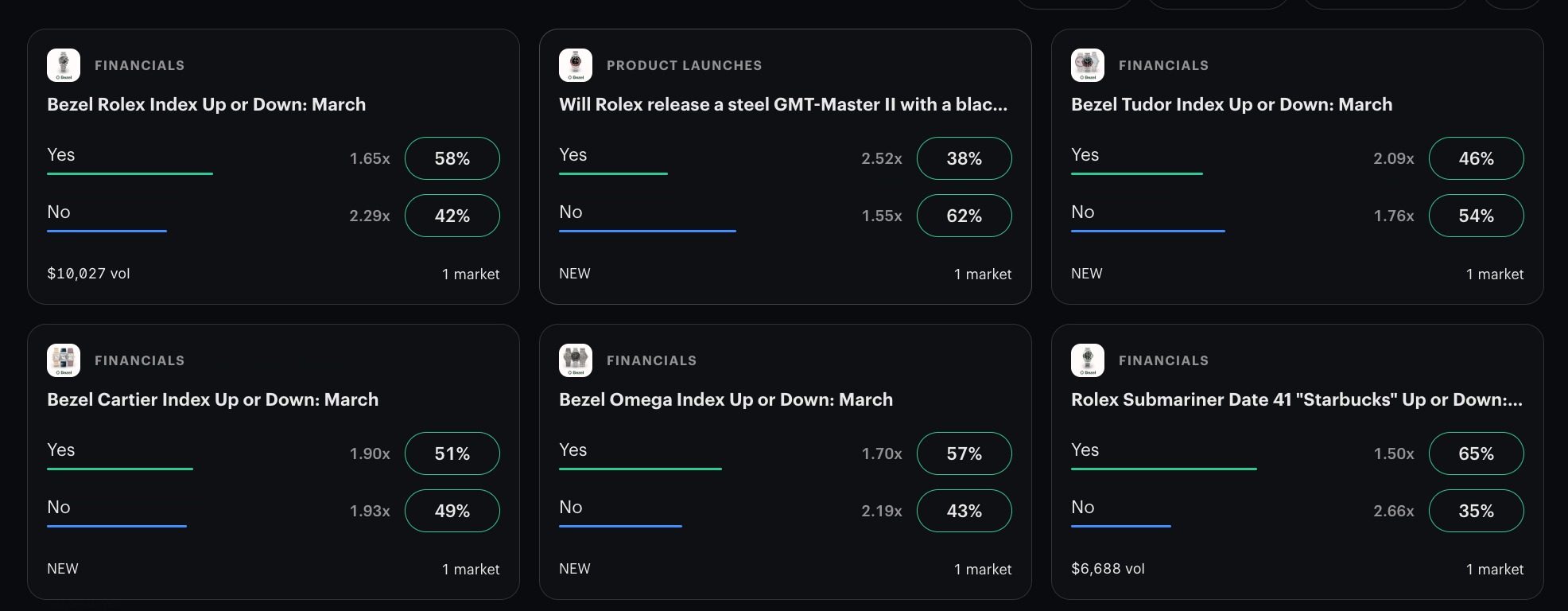

Kalshi launched Watch Futures with two types of markets:

Quantitative: Bet on whether the price of Rolex, Tudor, Cartier, or certain models will go up/down;

Qualitative: Bet on whether watches like the Rolex GMT “Pepsi” will be released or discontinued.

Here’s what it looks like:

I talked to Bezel co-founder Quaid Walker, who gave two justifications for Watch Futures: (1) transparency, and (2) democratization:

“Watch pricing is opaque,” he said. “Folks who are insiders and know where to look can aggregate their own data, but the market could benefit from more transparency.”

“We’re also excited because people are really passionate about watches, but the barrier to collecting is so high.”

I mostly agree—certainly on the first one.3 At their best, prediction markets can surface information and create more transparency. That said, this argument almost presupposes that insider trading is happening on these platforms, which is…frowned upon…in regulated financial markets.

But two days after launch, what’s actually happening in these Watch Futures?

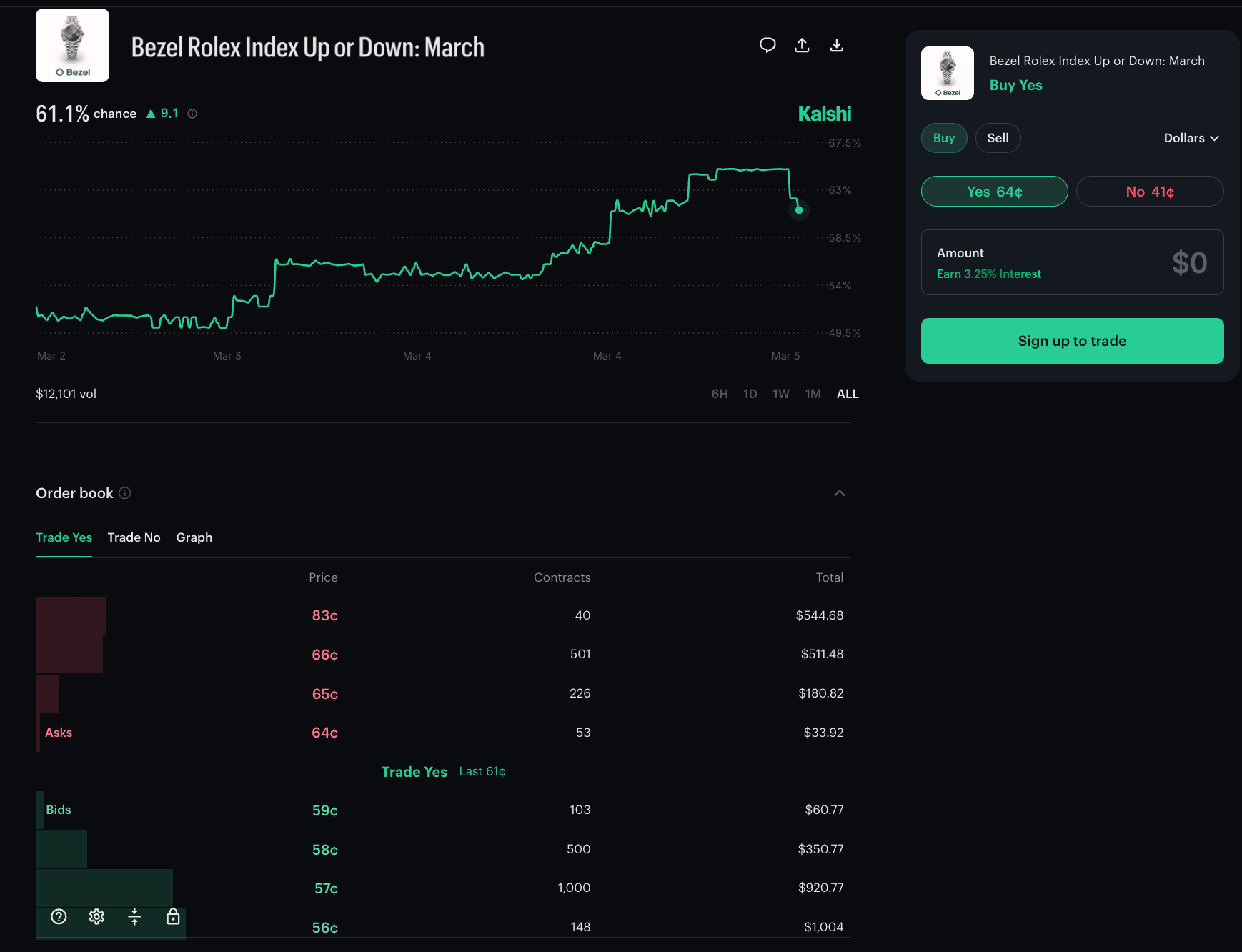

Let’s take a closer look, starting with the most popular market, the Rolex Index:

Notice that large bid-ask spread: That’s a 5¢ bid-ask spread—a healthy, liquid market would have a 1¢ spread. And the order book is super thin at those prices: Just $34 of contracts at the lowest ask (64¢). In other words, if you wanted to bet even just $34 on “Yes,” you’d move the price by one cent.

For the first two days, Kalshi subsidized the experiment. A few of the Watch Futures markets were part of its “rewards pool,” which incentivizes market makers and investors to provide liquidity. It kept the spread narrow and liquidity higher. But that ended on March 5.

Now, the Rolex market is mostly untradeable. The cost of the spread alone is higher than any realistic monthly gain in Rolex value. Meanwhile, if you wanted to buy just $1,000 of “Yes,” you’d move the price almost 20¢ (notice how there’s only $725 of contracts from 64-66¢ before jumping to 83¢).

It’s the same story for other markets: Cartier, Tudor, Rolex, the Starbucks Submariner.

Contrast it with a healthy, active market like for the Democratic presidential nominee to see the difference.

Let’s look at one more market

For whether Rolex will discontinue the steel GMT-Master II Pepsi this year:

The liquidity story is even worse. While the spread for “Yes” trade looks like 1¢, it’s paper thin (left). There are just $6 of bids at 83-84¢. If you wanted to sell a "Yes" position of any meaningful size, the "real" bid is down at 77¢. This means a collector trying to exit just a $500 position would take an immediate 8% haircut to find enough buyers. The “No” side is essentially a ghost town (right).

Market movers: With such a thin order book, anyone can completely move the market with ~$1,000—whether you’re an unwitting retailer trader or wannabe market manipulator.

Even if you won, you lost. Imagine you made a $500 bet on “Yes” at 68¢ yesterday. Today, the price is 84¢—you made a good bet. But, there aren’t enough bids for you to get your money out at 84¢. If you sold all $500 of contracts, you’d immediately take the price down to 77¢, shrinking your “profit” by more than half.

You’re stuck. Rich on paper, but you have to take a discount now, or wait until the market finally resolves to get your money out. It’s not a market, it’s more like a party where the music cut out, but people can only file out the door one at a time. Which introduces a final issue:

It’s not like Rolex announces when it discontinues watches. There will be no decree from Geneva that the “GMT-Master II Pepsi is discontinued.” That means you could be caught in a limbo where it’s technically removed from Rolex’s website, but there are still reported deliveries of a watch. Does that mean that GMT-Master production is discontinued? That’s for Kalshi to decide.4

That’s how these qualitative markets resolve (or don’t); the quantitative markets resolve on Bezel’s proprietary data, which introduces its own potential issues.

Add in that the r/kalshi subreddit is basically users complaining about how they weren’t paid out. I find the rules determining the Watch Futures markets opaque and ambiguous, which opens the door for not getting paid out on what you might see as a technicality.

Remember Unpolished collecting rule #21: When it’s time to sell, liquidity is as important as market price.

Rule #21 applies to financial markets even more than watches. While a Pepsi GMT isn’t the most liquid thing in the world, it’s more liquid than a Kalshi contract for whether or not the Pepsi GMT will be discontinued.

You could say: Yea, but it’s only day three. Give the market time to grow. Fair enough, but you could also argue that the launch might be the biggest marketing push these markets get. When else is a Kalshi x Bezel tweet going to get 2.8m views?

Taking the under

There are other issues with prediction markets—cultural, societal, legal. I’m not going to lecture young men about how they should or shouldn’t spend their time or money. There’s plenty of hand-wringing going on elsewhere; ScrewDownCrown has a balanced breakdown for how this might apply to watches.

Remember how I said this follows experiments with other collectibles like Pokémon and Labubus? As of today, I couldn’t find any active markets for those from at least the past month.

So who knows if this’ll last.

I did find one collectibles market with high volume: What will Logan Paul’s Pikachu go for at auction? (Another sentence that makes no sense to Mrs. Unpolished.)

It reminded me of being in Geneva during last fall’s auction season: All anyone wanted to talk about was how much we thought that steel Patek 1518 would sell for.

It’s kinda like sports: No one really bets on how many games the Seahawks will win in 2025; they bet on whether they’ll beat the Patriots in Super Bowl LX. We love to talk about the biggest and the best.

I could see a market around big watch sales like that being interesting, or, at least, fun. Is it good for society? That’s another conversation.5

Collectors as Lab Rats

Watch Futures are being marketed as “for collectors,” making the market more transparent and accessible.

But really, collectors are the test subjects. For the 48 hours after launch, Kalshi offered rewards to high-frequency traders, subsidizing market liquidity. When those rewards left, so did the money, and now we’ve got incredibly thin and fragile markets.

Presumably, Kalshi is trying to use these cultural assets to hook us into its wider ecosystem of finance/sports/entertainment betting. Come for Rolex, stay for the Oscars, S&P 500, or the Ayatollah.

All of it—crypto, NFTs, sports, prediction markets—feels borne from this financial nihilism young people feel, that there’s no way to make it in this world, so might as well take a turn at the casino. A sense that the system is “rigged,” ignoring that prediction markets can be just as rigged.

Meanwhile, if they can get enough of us to actually bet on Rolex, they’ve got a useful data set they can sell back to institutions—auctions, dealers, insurers, retailers.

It’s a brilliant business model if it works, and it just might—but this says more about where society has gone wrong than anything Kalshi or Bezel have done.

Unpolished is the newsletter for watch collectors and a top-20 Fashion & Beauty Substack. Subscribe to get it in your inbox for free:

Funny enough, the CEO of Guggenheim Partners (Mark Walter) owns the Dodgers and Lakers. The President (Andrew Rosenfeld) owns Urban Jurgensen.

It’s not as bad as betting on deposing world leaders, but you get the idea.

The last one feels like it makes a few logical leaps, but whatever. I get the premise that trading a $1 options contract is easier than buying a Pepsi GMT-Master.

Hell, if I really wanted to lawyer it, I’d point out that the contract doesn’t even refer to the specific reference (126710BLRO), and that this lack of specificity leaves more room for ambiguity.

No, it’s not.

You make a great point that Quaid Walker seems to miss: this is explicitly NOT for collectors. This is for speculators who want the financial returns of the watch without collecting.

In theory, if there was enough liquidity to divert this crowd from flipping allocations, it’d actually be healthy. But disappointingly enough this is not designed as a mechanism to do that. It’s designed to predate on ill informed retail investors

It’s gambling. Gambling is not a financial product. It is just gaming. The system is mathematically rigged against speculative betters over the long term and I don’t understand what’s the economic utility of it other than recreational game of chance.